Global ad spends in 2018 strongest since 2010

By M4G Bureau - June 22, 2018

Global ad spend remains strong thanks to robust economies -- US +6.4%, China +10%, Russia +12%, India +12.5%; The only traditional media category to show moderate growth in 2018 will be OOH

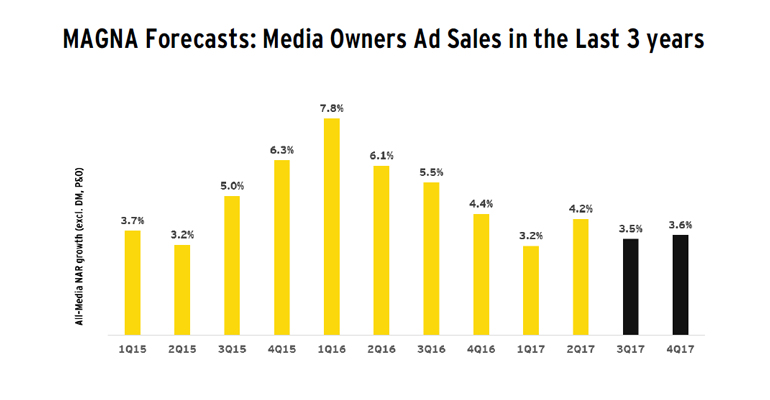

Media intelligence arm of IPG Mediabrands, MAGNA, in its Spring 2018 Update Global Advertising Forecasts states that media owners’ net advertising revenues (NAR) will grow by +6.4% to $551 billion in 2018 in 70 countries -- the strongest growth rate since 2010.

Media intelligence arm of IPG Mediabrands, MAGNA, in its Spring 2018 Update Global Advertising Forecasts states that media owners’ net advertising revenues (NAR) will grow by +6.4% to $551 billion in 2018 in 70 countries -- the strongest growth rate since 2010.

The 2018 growth (+6.4%) is an acceleration from 2017 (+4.5%), mostly due to the $5 billion of incremental ad spend generated around cyclical events in 2018 (US Mid-Term elections, FIFA Football World Cup, Winter Olympics). Neutralising the cyclical revenues, the 2018 growth would be +5.5%, in line with 2017.

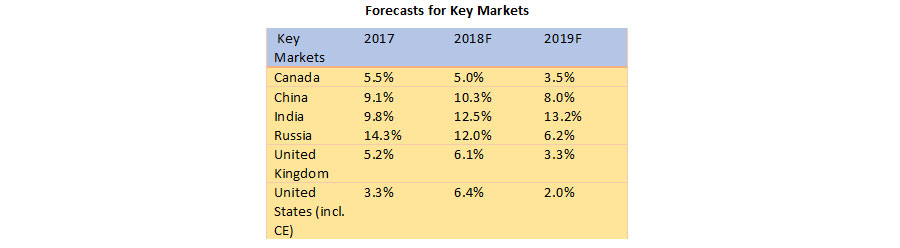

Global ad spend remains strong thanks to robust economies (US +6.4%, China +10%, Russia +12%, India +12.5%) and convalescent/recovering economies (Latin America +10%, Middle East +9%). Western Europe lags behind due to low economic growth and political uncertainty (+4.1%).

69 of the 70 ad market analysed by MAGNA are expected to show some level of growth this year, with Singapore the only market forecast to shrink this year. The fastest-growing regions in 2018 will be Central & Eastern Europe (+9.2%) and Latin America (+9.6%), followed by Asia-Pacific (+6.9%) and North America (+6.3%).

Digital advertising sales will grow by +15.6% in 2018 to reach $250 billion or 45% of global advertising revenues. Mobile ad sales reached half of total digital spend last year, and will increase to 62% of total digital spend this year. Digital will represent half of the world’s total advertising sales by 2020.

According to Vincent Létang, EVP, Global Market Intelligence at MAGNA and author of the report: “Global Advertising Spending is going to expand by the strongest growth rate since 2010 this year, as several of the largest markets – including the US, Russia and China – experience robust economic growth. Many consumer packaged goods and automotive brands are freezing or cutting ad expenditure, which hurts the revenues of traditional media types, while digital media, used by millions of small and local advertisers, seems to be immune from slow-down so far. Linear television will enjoy modest growth in most markets however, as cyclical events bring incremental budgets and strong pricing (CPM inflation), offsetting shrinking volume (ratings decline).”

Linear television ad revenues will grow again in 2018 (+3% to $185 billion), thanks to the return of even-year cyclical events, despite the continued, worldwide erosion of reach and ratings. Without the incremental even-year ad sales, TV would be just flat this year (+0.4% globally, -1.4% in the US).

Global Digital advertising sales (display, video, search, social) will grow by +15% this year, to $250 billion, slowing only slightly from 2017 (+18%), while offline ad sales (linear television, print, broadcast radio, out-of-home) will decrease by -0.2% to $300 billion. Digital media sales will represent 45% of total ad sales by the end of 2018 and MAGNA anticipates that it will reach 50% of global ad dollars by 2020. It will reach that milestone this year in the US, while the market share of digital media sales is already beyond 60% in markets like the UK or Sweden.

Digital ad spend will continue to be driven by Social (+31%) and Video (+27%) formats this year. Search will grow by +14% to $47 billion and remains the largest ad format.

Despite the scale reached by digital media spend and the controversies that hit some of the media owners in the first half of 2018, digital ad spend has showed no signs of slow-down yet. The combined advertising revenues of Facebook and Google grew by +31% year-over-year in the first quarter of 2018. Nevertheless MAGNA does anticipate a mild slow-down in the second half of the year but so far, spending from small, local, direct advertisers – often re-allocated from below-the-line marketing channels (direct mail, yellow pages) – continues to grow quickly, offsetting any slow-down in the spending from brand advertisers.

The only “traditional” media category to show moderate growth in 2018 will be Out-Of-Home. Global NAR is forecast to grow by +3.4% to $33.5 billion. OOH does benefit from cyclical events but the main driver remains the roll out of digital OOH inventory. DOOH NAR will grow by +16% this year to reach $5.7 billion as new airports, malls and transport system become available for media buying this year. For instance the “old” DOOH system in the London underground is about to be upgraded and expanded, and thousands of screens are to be rolled out in the New York Subway.

Other media categories will struggle to various degrees this year as they don’t benefit from the pricing power and cyclical drivers of national television. Global Print NAR will decrease by -11% to $54 billion. Radio ad sales will decrease by -2% to 28 billion. This reflects legacy ad sales only (paper, linear broadcast spots).

Stay on top of OOH media trends