Global media consumption grows at accelerated 2.7% in 2022: PQ Media report

By M4G Bureau - April 10, 2023

Media consumption growth was fuelled by new, more compelling original content releases, various international sporting events and federal elections in several of the top 20 global media markets.

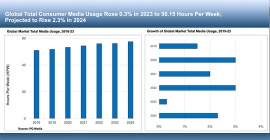

Global consumer media usage, including all digital and traditional media channels, grew at an accelerated rate of 2.7% to an average of 55.81 hours per week (HPW) in 2022, following a sharp deceleration in time spent with media growth to 1.7% in 2021, which came on the heels of the fastest increase in media consumption in 15 years in 2020 with a pandemic-fuelled surge of 3.3%, according to research released by PQ Media, a leading provider of media econometrics.

Consumer media usage grew at a faster pace in 2022, fuelled by new, more compelling original content releases, various international sporting events and federal elections in several of the top 20 global media markets. Foremost among the sporting events were the FIFA World Cup coverage from Qatar (almost 3.5 billion viewers in 2022); the Winter Olympics from China; and hockey’s World Championships in Finland. In addition, the US featured a number of hotly contested federal elections late in the year, according to PQ Media’s 10th annual Global Consumer Media Usage Forecast 2023-2027.

The accelerated gain in 2022 was slightly higher than anticipated and more in line with pre-pandemic levels for an even year. In some major markets, such as China, COVID restrictions had to be tightened due to sporadic breakouts that required some consumers to stay home again.

However, select media also exhibited a slowdown in use in the second half of 2022 as the global and US economies lost momentum due to myriad macroeconomic challenges, including high inflation, continuing inventory and supply chain issues, energy supply shortages, increased interest rates and the emergence of recession fears. This led middle- and lower-income consumers to cut discretionary spending on media and entertainment, from books to streaming media and other digital devices and related content.

Among the major trends and drivers that emerged during this year’s analysis is that media usage is reverting back to pre-pandemic trends that included a benchmark point when traditional and digital device penetration would reach saturation. That was interrupted by pandemic lockdown measures that shook up the global media economy in 2020 in such a way that secular trends driving down media usage growth in key segments were reversed, as executives built their home offices and students were not able to socialise with friends outside the home.

With the advent of vaccines being administered, many executives have returned to their corporate offices and students to their classroom buildings, that includes extra-curricular activities. As such, in most mature markets, such as the United States, Germany and Japan, will register declining media usage in odd years when there are only a handful of international sporting events and political campaigns to drive media consumption.

“As early as 2018, we began to see trends emerging that portended a looming saturation point, at which time the device purchase, data plan fees, content usage trends, longer upgrade cycles, etc., baked into our forecasts for several years were now coalescing into a strong secular shift, and our econometric intelligence is currently indicating market conditions, growth opportunities and headwinds, key economic variables, among other data, we’re now very close to what PQ Media projected three years ago. In that the macroeconomic trends further support that this key market driver has reached fruition,” said PQ Media CEO Patrick Quinn. “Among the anchors slowing down media consumption is a drop in digital device shipments, leading to mobile media consumption rising at a mere single-digit rate in 2023 – the first time this has ever happened.”

Among other key findings from the report:

The average global consumer spent 7.97 hours per day with media in 2022, up from 7.14 hours in 2017 (in some markets, like Japan, daily media usage exceeded 12 hours per day);

Digital media has been gaining approximately a 2% share annually in total usage over the past five years, with consumers spending 35.3% of their time with digital media in 2022, up from 25.5% share in 2017 (in four markets, like South Korea, digital usage exceeded 50% in 2022);

Ad-supported media accounted for 53.7% of time spent in 2022, down from a 58.5% share in 2017, with global consumer-driven media usage to exceed 50% for the first time in 2027 (in the U.S., this reflection point was reached in 2018); The Greatest Generation (born before 1945), use media the most, averaging 90.08 hours per week in 2022, while Millennials (1983-1996) use digital media the most, at 23.49 hours per week, and i-Gens’ (1997-2012) digital usage exceeds 50% (51.1%) (in most mature markets, Millennials also use digital media more than 50% of the time);

Television (including live, digital, streaming and over-the-top (OTT) video) remains the most used of the 11 media platforms that PQ Media tracks, reaching 27.78 hours per week in 2022, while home video posted the fastest growth, up 11.5% (fuelled by consumers returning to movie theatres and more blockbuster hits being released);

Mobile video posted the highest gain of the 22 digital channels that PQ Media monitors, up 18.6% in 2022, while OTT video is the most used digital channel at 7.27 hours per week (but only six digital media channels exceeded a 10% growth during the year);

Traditional media usage was at in 2022, with only print books, over-the-air (OTA) radio, and print newspapers posting growth during the year, some of which was fuelled by coverage of the Ukraine conflict (but overall traditional media usage will begin to decline in 2023 and is not expected to post positive growth ever again);

“As consumers continue to cut discretionary spending in 2023 amid current consumer sentiment and other key macroeconomic conditions, media companies have had to readjust prot projections and act accordingly. For example, streaming video services reported in 1Q23 that they're cutting back production schedules of original content, other than live sports, as the average consumer is dropping to only four subscriptions OTT services from six last year, shaving off excess content subs that were added during the apex of the pandemic in 2020-21," said PQ Media's Quinn. "As the gold rush to cash in on what appeared to be a sweeping secular shift to streaming video, audio, news, entertainment and sports was, ultimately, a non-recurring, short-term, cyclical event with resulting blowback implications on the broader economy.

Stay on top of OOH media trends

_440_851.png)

_140_270.png)